An Opinion Editorial By: Riker Farmer

In cities with high population growth a highly predictable surge in housing prices occurs. Vancouver and Toronto were hit especially hard by Canada’s recent population growth. Edmonton, on the other hand, has seen larger increases in population yet housing costs remain level and have even taken a slight drop since 2024.

Healthy vacancy rates prevent rent hikes

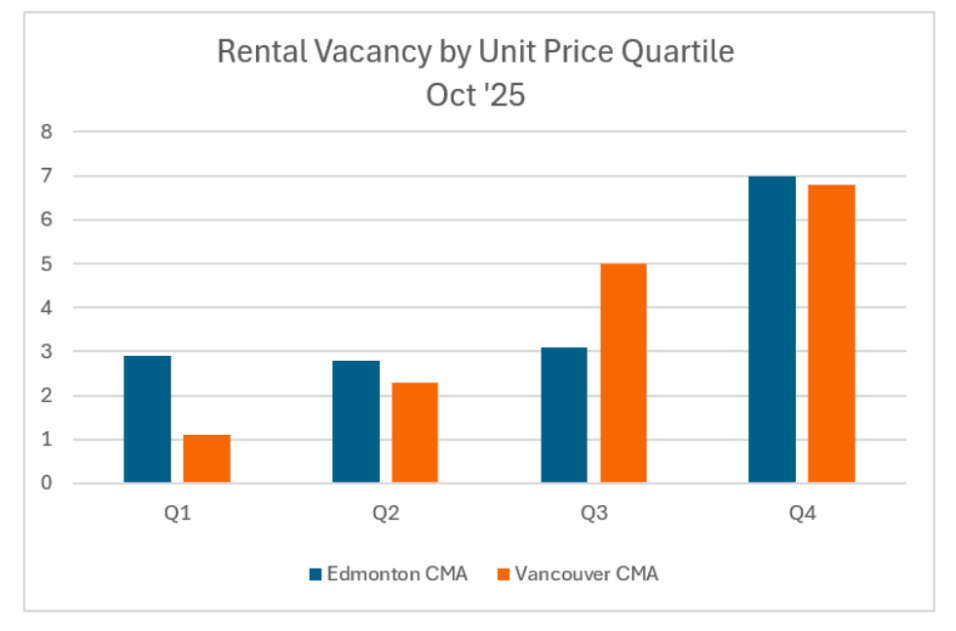

Edmonton grew by 5.7% and 3.4% in 2024 and 2025 respectively. In Vancouver, similar growth pushed the cheapest rentals to near zero vacancy. Edmonton has managed to absorb similar growth in demand without causing strain on the housing supply. As of last October, vacancy rates in Edmonton across the cheapest 75% of rentals were hovering around a healthy 3%. At this level of vacancy, there is a balance in the leverage between landlords and tenants, making rent hikes unlikely.

Source: CMHC 2025 Rental Market Report

In other markets that have seen Edmonton’s magnitude of population growth, the vacancy rate in the premium (Q4) quartile almost always spikes first, with a gradual filtering down. This is largely because newer builds demand rent premiums well above the median rent in order for the development to pencil out, driving middle-income renters toward lower-tier units that remain affordable for them.

This structural mismatch in places like Vancouver is due in large part to zoning restrictions that permit density only in areas with natural premiums like near transit and along major commercial corridors. The only new housing supply provided are large site projects with tremendous fixed costs and risk premia. In the developer’s pro forma, the math only works out when the rentals are priced at a premium.

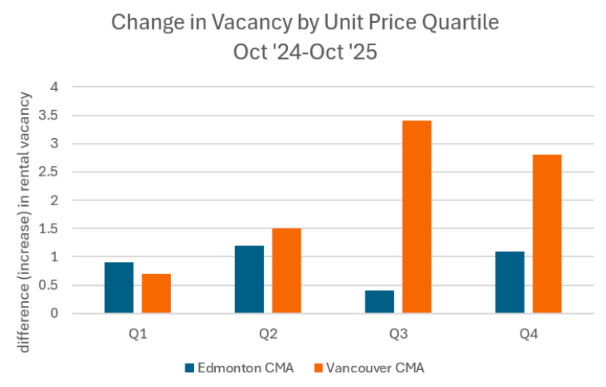

Negative absorption dominated by below-median rentals

Instead of the downward filtering pattern seen in Vancouver, Edmonton’s steepest increase in vacancy is actually occurring in its bottom 50%. When analyzing CMHC1 data to map the year-over-year changes in these markets, the vacancy increase in Vancouver is dominated by the top 50%. In Edmonton, the cheapest 50% of rentals having a higher increase in vacancy than the top 50% is the exact mechanism that is causing rents to drop.

Source: CMHC 2025 Rental Market Report

Zoning reform removed barriers to small-scale infill

The main driver of Edmonton’s affordability is a rise in missing-middle construction, made legal in 2024 as part of its Zoning Bylaw Renewal.

The old zoning framework allowed single detached homes in the RF1 zone, semi-detached homes in the RF2 zone and rowhomes up to 1 unit per 150 m2 in the RF3 zone. The zoning bylaw, in conjunction with Area Redevelopment Plans, strictly dictated how and where developers can add density.

The full rewrite of Edmonton’s Zoning Bylaw, which took effect at the beginning of 2024, allowed by-right 1 unit per 75 m2 which is capped at 8 units for a midblock lot. Additionally, instead of controlling the exact type of residential use (single family/semi-detached), the city now allows any residential use. This allows developers and neighbourhood-driven demand to decide the form of housing it desires.

Removing arbitrary parking requirements cut development costs

The City also removed minimum parking requirements in 2020, switching to Open Option Parking to allow market forces to determine how much parking a property needs. A semi-detached home may demand a heated 2 car garage per unit in order to position itself, but a small 8-unit apartment building near transit will likely do well with an uncovered 3-to-4 car concrete pad off the rear lane. Instead of applying a broad stroke of “one stall per unit” across all types of residential buildings, developers pick and choose based on what adds the most value to their target demographic.

Unlocking densification through low-cost and low-risk development

Small-scale infill developments also operate within Part 9 of Alberta’s Building Code, making permitting and construction costs much lighter, thus creating a very cost effective way of delivering more units to the market. This reduces a lot of the costs associated with residential development, and these savings get passed on to renters due to a high degree of competition. New developments in Edmonton can get away with asking for far less in rent than the typical premium that large-scale infill needs in order to pencil out, which allows missing-middle housing to be priced in a mid-tier quartile instead of competing in the luxury space.

The delivery mechanism of small-scale infill also introduces a critical time advantage. Instead of the multi-year horizons required for large developments, missing-middle projects deliver finished units to the market within 12 to 15 months. This compressed cycle drastically reduces interest rate risk and carrying costs. Small-scale developers can accept a lower rate of return due to less uncertainty.

Vacancy relief for the cheapest rentals

The result of all this new missing-middle development is that the cheapest 75% of rentals are becoming highly stable. Instead of middle-income renters being pushed into the lowest quartile during a population growth surge, Edmonton’s supply is steadily keeping up with exactly what the market demands. This allows the vacancy in the cheapest 75% to hover comfortably around 3%.

Japan’s precedent for gentle density

It is often suggested that Edmonton’s affordability is due to nearly endless cheap land nearby and that the nature of Toronto and Vancouver’s spatial constraints make them inevitably unaffordable. But Edmonton’s current affordability advantage actually comes from its ability to grow upward, not outward.

Looking internationally, Japan has a very similar regulatory framework of bottom-up, demand-driven density. In the 1970s, Japan nationalized the zoning code and consolidated their zones down to just 12 core “use categories.” Just as Edmonton is doing, bottom-up gentle density allows developers to deliver more housing where there is demand for it. Today, Japan has the most affordable rent of any developed country.

Japan largely achieves affordability by allowing space for every form of housing the market demands. Hyper-affordable micro apartments in Tokyo’s suburbs can be rented for as little as CA$300, because there is an environment for a developer to be able to easily reposition an existing building to something the market demands.

Thirty months ago Edmonton officially reformed its regulatory environment allowing cheap and cost effective density to be added and respond to demand. As a result, the most affordable units can remain affordable, slowing or preventing housing scarcity. Edmonton’s Japan-like approach shifted to the North American context is now the blueprint for municipalities that take affordability seriously.